Capital cost allowance for EVs – 2025 fiscal year

April 15, 2026

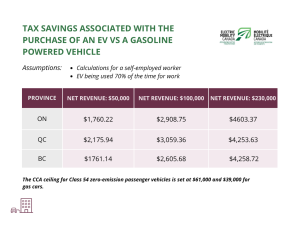

For the 2025 fiscal year, Canada’s Capital Cost Allowance (CCA) rules continue to provide enhanced depreciation for eligible zero‑emission vehicles (ZEVs), strengthening the business case for electric vehicle adoption.For the 2025 fiscal year, Canada’s Capital Cost Allowance (CCA) rules continue to provide enhanced depreciation for eligible zero‑emission vehicles (ZEVs), strengthening the business case for electric vehicle adoption.

Under the accelerated CCA framework, businesses can claim up to 55% of the cost of an eligible electric vehicle (class 54) in the first year the vehicle is available for use. This accelerated write‑off applies to qualifying passenger EVs and to medium‑ and heavy‑duty electric vehicles used for commercial purposes, subject to vehicle class and applicable cost limits.

THIS IS FOR INFORMATIONAL PURPOSES ONLY. PLEASE CONTACT A FINANCIAL PROFESSIONAL IF YOU HAVE ANY QUESTIONS REGARDING THE CCA FOR EVs. PLEASE DO NOT CONTACT EMC STAFF ON THIS MATTER AS WE ARE NOT QUALIFIED TO PROVIDE INDIVIDUAL FINANCIAL ADVICE.

THIS IS FOR INFORMATIONAL PURPOSES ONLY. PLEASE CONTACT A FINANCIAL PROFESSIONAL IF YOU HAVE ANY QUESTIONS REGARDING THE CCA FOR EVs. PLEASE DO NOT CONTACT EMC STAFF ON THIS MATTER AS WE ARE NOT QUALIFIED TO PROVIDE INDIVIDUAL FINANCIAL ADVICE.